It's common knowledge that the 4% rule applies to all things. But how do you figure it? In this article, we will explore the 4% rule, how to invest, and create a simple budget to save for retirement. Then we'll explore other retirement savings options, such as investing into a brokerage account. We'll also explore Social Security income substitution rates and a hypothetical scenario for retirement. Once you know what your retirement deficit is, you can figure out how much you need to save to reach your goal.

4% rule

The 4% retirement savings rule was developed using historical data from 1926 to 1976, with particular attention to the severe market downturns of the 1930s. This approach is intended to allow for inflation even though the target inflation rates are only two percent each year. The current low rate inflation makes this approach unsuitable for most investors. Investors must consider all options and include fixed-income securities as well as investments.

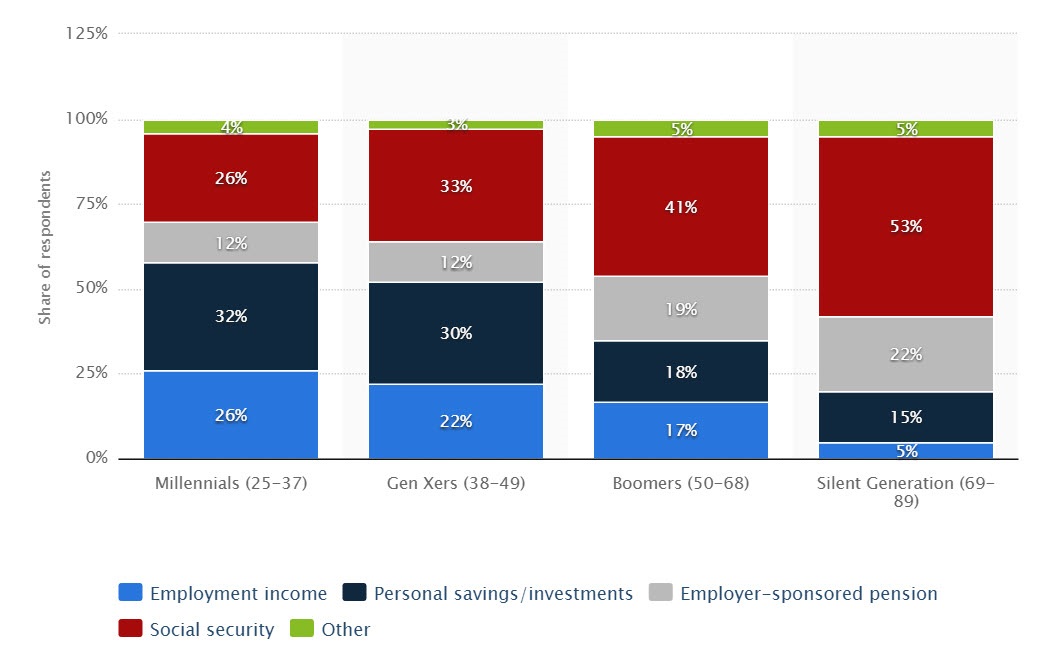

Social security income replacement rate

To calculate how much to save for retirement based on your Social Security income replacement rate, you need to know your income before retirement and your current spending levels. The lower your income replacement rates, the higher your preretirement income will be. You should aim to replace 75% your income when you retire. Save up to $106,000 if your annual income is $70,000. Aim to replace at minimum 90% of your income after retirement for households with less than $70,000.

Investing in a brokerage account

Many investors are hesitant to invest in a brokerage account for retirement, and for good reason. Brokerage accounts do not have contribution or income caps, unlike IRAs and 401(k). A brokerage account offers a variety of investment options, including stocks, bonds and publicly traded companies that are linked to commodities. Investors must also consider their time horizon, risk tolerance, and financial goals before investing.

Create a budget to help you save for your retirement

A budget is essential before you can start saving for retirement. Take a look at your monthly expenses and compare them with your income. Add fun expenses to your budget and save the rest. It will make the transition to retirement much simpler if you have a budget. If you're still working, make sure to use your old job as a reference. Your job isn’t the same without your experience!

Save for retirement with seriousness

It's a great time now to start saving for retirement, even though you may have not thought about it in your early 20s. You may be able save more money every month with fewer expenses. You might be able save more. So a modest goal of $25 per calendar month in your 20s could make a significant difference for the future. If you get started early enough, you will have enough money when you reach sixty.

FAQ

How much do I have to pay for Retirement Planning

No. These services don't require you to pay anything. We offer free consultations that will show you what's possible. After that, you can decide to go ahead with our services.

What is risk management in investment management?

Risk management is the act of assessing and mitigating potential losses. It involves the identification, measurement, monitoring, and control of risks.

An integral part of any investment strategy is risk management. The objective of risk management is to reduce the probability of loss and maximize the expected return on investments.

These are the key components of risk management

-

Identifying the risk factors

-

Monitoring and measuring risk

-

Controlling the Risk

-

Managing the risk

Is it worth having a wealth manger?

A wealth management service can help you make better investments decisions. It should also advise what types of investments are best for you. You will be armed with all the information you need in order to make an informed choice.

There are many factors you need to consider before hiring a wealth manger. Is the person you are considering using trustworthy? If things go wrong, will they be able and quick to correct them? Can they easily explain their actions in plain English

How old should I start wealth management?

Wealth Management should be started when you are young enough that you can enjoy the fruits of it, but not too young that reality is lost.

The sooner that you start investing, you'll be able to make more money over the course your entire life.

You may also want to consider starting early if you plan to have children.

Savings can be a burden if you wait until later in your life.

What are the benefits of wealth management?

The main benefit of wealth management is that you have access to financial services at any time. You don't need to wait until retirement to save for your future. It also makes sense if you want to save money for a rainy day.

To get the best out of your savings, you can invest it in different ways.

You could, for example, invest your money to earn interest in bonds or stocks. Or you could buy property to increase your income.

If you hire a wealth management company, you will have someone else managing your money. You don't have the worry of making sure your investments stay safe.

Statistics

- As of 2020, it is estimated that the wealth management industry had an AUM of upwards of $112 trillion globally. (investopedia.com)

- A recent survey of financial advisors finds the median advisory fee (up to $1 million AUM) is just around 1%.1 (investopedia.com)

- If you are working with a private firm owned by an advisor, any advisory fees (generally around 1%) would go to the advisor. (nerdwallet.com)

- Newer, fully-automated Roboadvisor platforms intended as wealth management tools for ordinary individuals often charge far less than 1% per year of AUM and come with low minimum account balances to get started. (investopedia.com)

External Links

How To

How to invest after you retire

Retirement allows people to retire comfortably, without having to work. But how can they invest that money? While the most popular way to invest it is in savings accounts, there are many other options. You could, for example, sell your home and use the proceeds to purchase shares in companies that you feel will rise in value. You could also take out life insurance to leave it to your grandchildren or children.

If you want your retirement fund to last longer, you might consider investing in real estate. The price of property tends to rise over time so you may get a good return on investment if your home is purchased now. If you're worried about inflation, then you could also look into buying gold coins. They do not lose value like other assets so are less likely to drop in value during times of economic uncertainty.